Investors are anxiously awaiting more details on the new US

Administration’s economic policies and priorities. Part of the

challenge is that the cabinet represents a wide range of views and it is not

clear where the informal power lies, or whose call is it. In terms of

economic policy, trade is being given priority. It is seen as

the key to the jobs and growth objectives.

There have been two initiatives: formally withdrawing for the

Trans-Pacific Partnership and indicating a desire to re-open NAFTA.

Neither one is surprising, but will likely nevertheless have far-reaching

ramifications. In the previous administration, the two issues were tied

together. NAFTA was understood to need updating, but rather than re-open

negotiations per se, Obama opted to include Canada and Mexico into the TPP would supplant NAFTA. For the Trump

Administration, not participating in TPP, exposures a greater importance of

re-opening NAFTA.

Asia.” It was a case of the flag following the trade. For more than 30-years, more goods cross that

Pacific than the Atlantic. Without TPP, the economic compliment, the

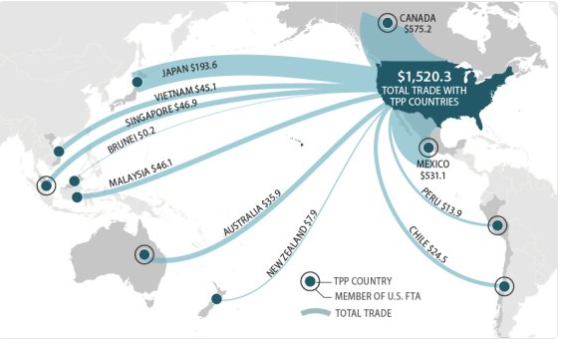

pivot to Asia take on a more militaristic tenor, which concerns China as a new form of containment. The Great Graphic

posted here is from Cato

Institute economists and depicts US trade with TPP

countries. In fairness, none of the last three candidates for

President (Trump, Clinton, and Sanders)

supported TPP. Australia and Japan are pushing to keep TPP without the

US, which is possible. It is also still possible that Trump negotiates a

bilateral free-trade agreement with Japan.

Many investors and economists do not seem to recognize the importance of

NAFTA. The trade that is

covered by the agreement accounts for almost a third of US trade, or roughly $1

trillion. In comparison, China is about a

sixth and the UK, which appears to be

moving higher in the queue under in the Trump Administration, accounts for a

tenth of US trade.

The auto sector has been a bit of a lightening rod for the new

Administration. Industry figures suggest that Mexican-made vehicles are made of about 40% American parts on

average. The US exported about $22 bln in vehicle parts to Canada in 2015

and $20 bln to Mexico. About 12% of US-made care are from Mexican

parts. A little over half of Mexican-made cars are exported to the US. GM, Ford, and Chrysler account

for almost half of Mexico’s light vehicle production.

President Trump seems to prefer bilateral agreements rather than the

large multilateral deals, like TPP. New bilateral agreements

could replace NAFTA, but a key element for the new Administration may be the

domestic content rules. Also, some

like Commerce Secretary Ross is also concerned about the VAT that Mexico has

lifted from 10% to 16%, and which is deductible for exporters. Ross has

argued this discourages exports and encourages manufacturers to build

production facilities in Mexico.

We have argued that for historical reasons US companies pursued a direct

investment strategy over the more traditional export drive. The

dollar was very strong under Bretton Woods, and as countries rebuilt after

WWII, direct investment was a way around protectionism. Under the

floating exchange rate period, direct investment was also embraced as a way to insulate companies from the new

volatility of currencies. If the

Trump Administration is going to discourage the direct investment strategy,

Corporate America will be undergoing a more dramatic re-orientation than many

seem to realize.